Energy Transition Leadership Briefing | May 2026

Opening snapshot

Australia’s energy transition visibly crossed an important threshold in May. Renewable energy has not only felled Liddell’s chimney stacks, but consumer electricity prices too.

The AER’s new Default Market Offer will give electricity price reductions of up to 5% for some consumers and 10% for some businesses across NSW, South Australia and southeast Queensland, the clearest regulatory evidence yet that large-scale renewables and batteries are beginning to structurally lower wholesale electricity costs.

At the same time, the transition is becoming more operationally complex. Data centres are emerging as a major new load source, hydrogen economics are being reassessed, and project pipelines continue to outpace actual delivery. Batteries are no longer “future infrastructure”, they are increasingly the mechanism stabilising prices, firming renewables and reshaping investment flows.

For years, the industry argued cheaper clean energy was coming. This month was one of the first times regulators effectively confirmed it.

Trendlines

- The “renewables lower prices” argument finally has regulatory evidence

The AER’s lower Default Market Offers are the strongest mainstream proof yet that rising renewable and battery penetration is reducing wholesale electricity costs for consumers.

Sources: AER, AFR - Data centres have become the new demand shock

AI and cloud infrastructure are no longer niche load issues. Transgrid’s 14 GW of connection enquiries and AEMO’s warnings around data centre demand growth are now reshaping transmission and generation planning.

Sources: AFR, AEMO - Hydrogen is being repriced downward

Budget cuts to Hydrogen Headstart and growing scrutiny around subsidy-backed projects show the sector moving from political enthusiasm to commercial reality.

Source: RenewEconomy - Isolation is driving battery uptake

Australia is racing ahead globally in battery uptake to being the third largest market globally, but Western Australia’s isolated grid has driven that uptake more than anywhere else. Battery discharge in WA has more than trebled to 300 GWh over the last year

Source: RenewEconomy, ABC News

- Distributed energy continues to accelerate

Household batteries and EV adoption are helping to continue the rooftop solar surge, here and globally. Source: CleanTechnica - Capital is concentrating into firming and scalable platforms

Investors remain active, but increasingly favour large battery portfolios, hybrid projects and assets with clearer revenue and connection pathways.

Sources: AFR, PV Magazine

Noteworthy announcements / projects

1) Default Market Offers fall as renewables and batteries reduce wholesale costs

What happened:

The Australian Energy Regulator cut Default Market Offers for many east coast households and small businesses, with reductions of up to 10% in some jurisdictions. Wholesale electricity prices softened as renewables and batteries displaced higher-cost generation.

Sources: AER, AFR

Why it matters:

This is arguably the most important public-facing transition signal of the year so far. For the first time, regulators are directly linking cleaner generation and storage growth to lower retail electricity costs.

2) Data centres emerge as a system-scale planning challenge

What happened:

Transgrid revealed it has received data centre connection enquiries representing roughly 14 GW of load, while AEMO warned data centre demand is rising faster than expected. Governments are considering rules requiring new data centres to offset demand with new renewable generation.

Sources: AFR, AEMO

Why it matters:

Data centres could become both a major driver of renewable investment and a political flashpoint around electricity affordability and grid access.

3) Akaysha positions as a major firming platform

What happened:

AFR Street Talk reported BlackRock-backed Akaysha could become Australia’s third-largest owner of firming capacity within 18 months as Macquarie Capital seeks a new investor.

Source: AFR

Why it matters:

Battery platforms are now being valued as strategic infrastructure portfolios, not standalone projects.

4) Big wind and hybrid projects are latest winners

What happened:

Results of CIS Tender 7 are out and Australia’s biggest wind projects, Origin’s 1.45 GW Yanco Delta and Windlab’s 1.4 GW Bungaban wind farms were successful, as were hybrid projects, although some solar only made it too.

Source: RenewEconomy

Why it matters:

The CIS is selecting and supporting projects, but the key is how many are getting to FID and into construction. Are revenue safety nets enough?

5) Offshore wind timelines continue to stretch

What happened:

Victoria committed new funding toward offshore wind enabling infrastructure, but Star of the South now expects completion no earlier than 2037.

Sources: AFR, Energy Magazine

Why it matters:

Offshore wind remains strategically important but is unlikely to solve near-term reliability or industrial demand growth challenges.

Hiring implications

The hiring market has been moderating since the strong post-COVID rebound with this financial year tightening around specific roles rather than pure project volume.

Roles getting scarce

- Battery revenue optimisation and trading specialists

- Grid integration and system-strength engineers

- Transmission and connection managers

- Data centre energy procurement leaders

- Senior project delivery executives (FID → energisation)

- Stakeholder and approvals leaders

Where demand is rising

- NSW: Data centres, transmission and firming assets

- Queensland: Large-scale wind, industrial energy demand and REZ delivery

- Victoria: Offshore wind preparation, transmission and grid infrastructure

- Western Australia: Mining decarbonisation, microgrids and long-duration storage

Typical organisational moves

- Developers separating origination from delivery functions

- Storage operators building trading and optimisation capability earlier

- Networks strengthening large-load connection assessment teams

- Greater executive scrutiny on delivery capability rather than pipeline announcements

The strongest hiring demand now sits exactly where the system is under pressure: integration, coordination and execution.

Policy pulse

1) Affordability narrative shifts materially

Lower Default Market Offers have given governments and regulators something the sector has lacked for years: observable evidence that renewables and batteries can reduce consumer electricity costs, not just emissions.

Sources: AER, AFR

2) Data centre regulation is coming

Governments are actively considering “full offset” models requiring data centres to back new demand with additional renewable supply.

Sources: AFR, AEMC

3) Reliability policy is becoming more pragmatic

Governments and market operators are increasingly prioritising dispatchability, system strength and reliability alongside decarbonisation targets. The policy conversation is shifting from “how fast can we replace fossil generation?” to “how do we maintain affordability and stability while doing it?”

Sources: AFR, AEMO, AER

Tech watch

- Thermal energy storage enters the industrial mainstream

Investment into thermal storage technologies continues to grow as industrial decarbonisation pathways expand.

Source: AFR - Residential battery integration becomes a systems issue

The next phase of household storage is orchestration, optimisation and grid interaction — not just installation growth.

Source: RenewEconomy - Grid-forming batteries continue scaling rapidly

Batteries increasingly dominate new connection pipelines and are expected to provide system strength services as coal generation exits.

Sources: RenewEconomy, AEMO

Data points

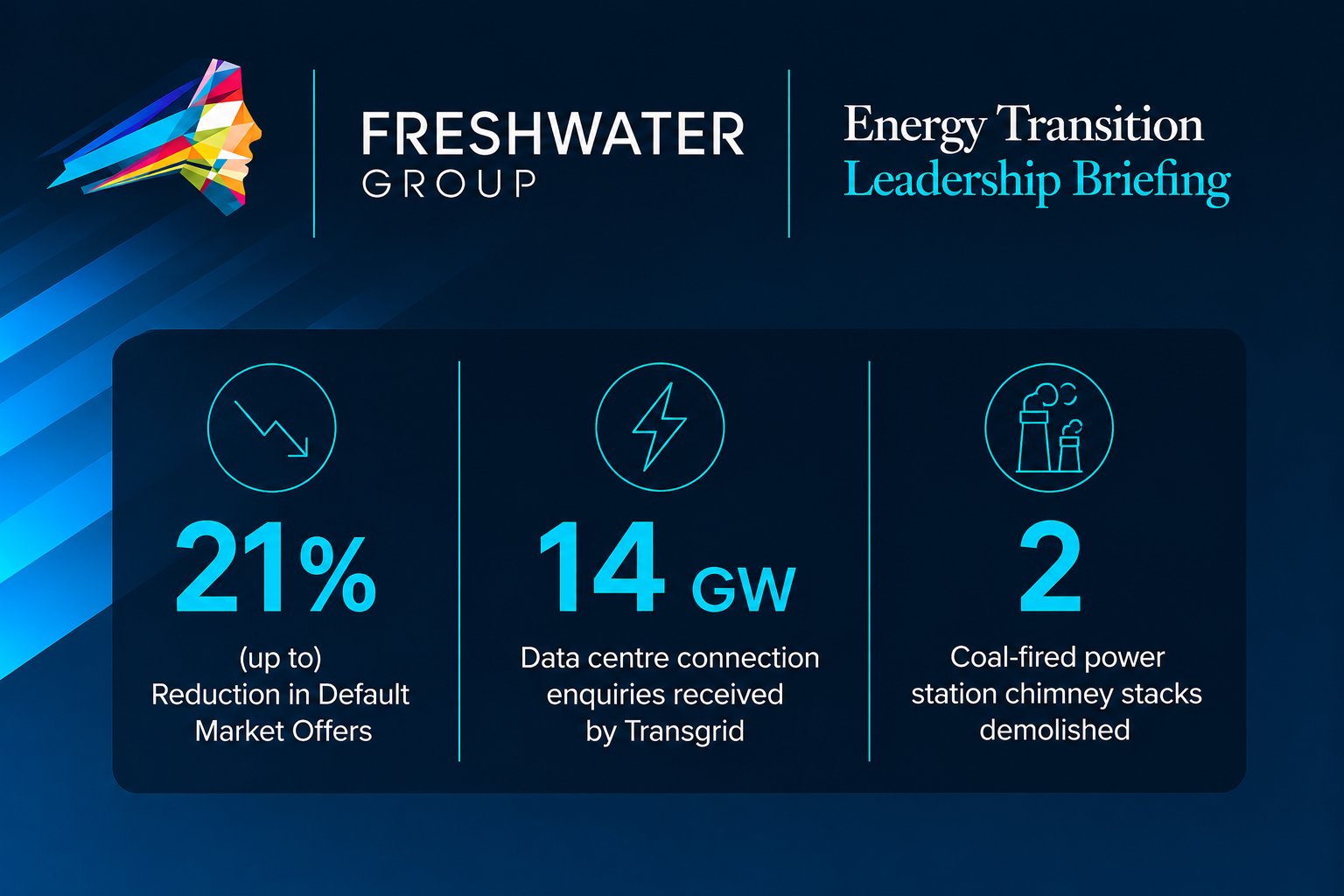

- 21% – Reduction in Default Market Offers for some NSW businesses, and up to 10% for some consumers under the AER’s latest determination.

- 14 GW – Data centre connection enquiries received by Transgrid, roughly equivalent to the entire NSW/ACT winter peak load.

- 2 – Coal-fired power station chimney stacks demolished at the former Liddell power station in NSW during May, marking one of the clearest physical symbols yet of Australia’s energy transition. The site is being redeveloped into a renewable energy hub anchored by a 500 MW battery.

Sources: The Guardian, The Australian

Watchlist for next month

- Data centre connection regulation and renewable offset rules

- Queensland storage and transmission decisions

- Institutional capital flows into large-scale battery platforms and hybrid assets

Final word

For years, the transition promised cheaper power, cleaner generation and more flexible energy systems.

In May, some of that stopped being theoretical.

Batteries helped lower prices. Data centres emerged as a genuine system challenge. Households accelerated back into distributed energy. And investors kept shifting toward firming, optimisation and scalable infrastructure.

The transition is no longer just about replacing generation.

It is about redesigning how the entire energy system works.

Prepared by Freshwater Group. Helping companies secure leadership and critical talent for the energy transition.

- Posted by Freshwater Group

- On May 29, 2026

- 0 Comment