Energy Transition Leadership Briefing | April 2026

Monthly Insights for Executives in Australia’s Clean Energy Sector

April 2026 Edition

Opening snapshot

April reinforced a shift in Australia’s energy transition from build-out to system integration. The volume of renewable energy and storage projects continues to surge, but the conversation is no longer about capacity alone. Instead, attention has turned to how the system actually performs under stress, how demand evolves alongside supply, and whether infrastructure can keep pace.

Batteries have moved from optional to essential, not just for firming but for system stability and market participation. At the same time, structural tensions are becoming clearer: negative pricing events are increasing, transmission remains a bottleneck, and policy settings are starting to materially shape investment outcomes.

Overlaying all of this is a new demand story. Electrification, data centres and industrial loads are beginning to reshape the demand curve, forcing a rethink of how the grid is planned and operated. The transition is accelerating, but the constraints are now just as important as the momentum.

Trendlines

Three trends sharpened in April.

- First, storage is now dominating the pipeline. AEMO data shows 67.3 GW of battery projects progressing through connection processes, underscoring that flexibility, not generation, is now the limiting factor in the system. (pv magazine Australia)

- Second, the market is shifting from managing peak demand to managing excess supply. In South Australia, grid-connected users were effectively paid to consume electricity nearly half the time during parts of 2025, driven largely by renewable oversupply. (pv magazine International) This dynamic is starting to influence investment decisions and industrial strategy.

- Third, the transition is increasingly constrained by infrastructure and coordination. AEMO’s latest planning signals confirm the system is changing faster than the networks and regulatory frameworks supporting it. (Energy Source & Distribution)

Together, these trends point to a transition entering a more complex phase, where orchestration matters more than raw capacity.

Point of view: The grid isn’t the bottleneck anymore. Coordination is.

For years, the narrative has been simple: build more generation, build more transmission, and the transition will take care of itself.

That story is now out of date.

April’s signals point to a system that is no longer constrained by renewable ambition or even capital. It’s constrained by how well the pieces work together. Oversupply events, curtailment, negative pricing and connection delays aren’t symptoms of underinvestment. They’re symptoms of a system that hasn’t caught up with its own complexity.

The uncomfortable implication is this: adding more capacity, on its own, may now reduce value rather than create it.

The winners over the next phase won’t be those who simply build more assets. They’ll be the ones who can optimise across portfolios, manage volatility, and extract value from increasingly chaotic market conditions.

In other words, the transition is shifting from an infrastructure race to an intelligence race.

Noteworthy announcements / projects

Major battery and storage expansion continues

AEMO connection data highlights the scale of battery development, with tens of gigawatts of projects moving through approvals. This signals a structural shift toward storage-led system design. (pv magazine Australia)

ARENA-backed microgrids for First Nations communities

New funding for community-led microgrids in the Northern Territory reflects a growing focus on decentralised energy models and social licence in the transition. (ESD News)

State-backed grid investment ramps up

A $1.4 billion fund to accelerate transmission and connections ahead of coal closures highlights the urgency of enabling infrastructure, not just generation. (Renew Economy)

Commercial and industrial demand growth accelerates

Expansion in data centres and electrified industry is emerging as a key driver of future load growth, reshaping the demand outlook and investment case for generation and storage. (pv magazine Australia)

First tower, first REZ

The first transmission tower has been erected in Australia’s first renewable energy zone, the Central-West Orana REZ, as it looks to come online by 2028. Energy Magazine)

Policy pulse

Policy focus is tightening around system efficiency and integration rather than just renewable targets.

Proposed reforms from the AEMC aim to reduce solar curtailment through improved planning frameworks and data transparency, potentially unlocking billions in system savings. (pv magazine Australia)

At the same time, broader policy debates are becoming more contested. Discussions around market design, network pricing and the effectiveness of mechanisms like the Safeguard Mechanism suggest that while policy direction remains broadly supportive of decarbonisation, the implementation is under increasing scrutiny. (Renew Economy)

Internationally, coordinated efforts to manage a transition away from fossil fuels continue, but domestic execution remains the critical factor for Australia’s trajectory.

Tech watch

The decarbonised process heat hard nut is getting cracked

Graphite Energy has secured $40 million in combined debt and equity funding to accelerate the rollout of its modular renewable industrial heat systems. (Ecogeneration)

Sodium-ion batteries scale up

Large-scale supply agreements for sodium-ion batteries point to a potential diversification away from lithium-ion, with implications for cost and supply chains. (Renew Economy)

Distributed solar integration technologies

New approaches to reducing rooftop solar curtailment and improving distribution-level visibility are emerging as critical enablers of high-penetration systems. (pv magazine Australia)

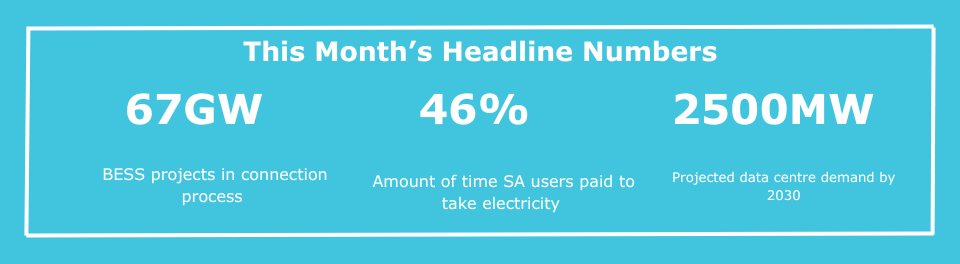

Data points

- 67.3 GW of battery storage projects progressing through NEM connection processes (pv magazine Australia)

- 46% of the time SA grid users were effectively paid to consume electricity during periods of oversupply (pv magazine International)

- ~2500 MW projected data centre demand by 2030, up from ~1050 MW in 2024 (pv magazine Australia)

Hiring implications

The hiring market is quietly pivoting in line with the system’s complexity.

Demand is moving away from pure development towards delivery and asset management roles with capabilities in integration, optimisation and system performance. Project Directors, Asset Managers, Grid Engineers, power systems specialists, and those with experience in storage and hybrid systems are becoming increasingly scarce.

There is also a growing need for talent that can operate at the intersection of energy and digital infrastructure, particularly as data centres and electrified industry reshape demand profiles.

At a leadership level, the shift is even clearer. Organisations are looking for executives who understand not just project pipelines, but how assets perform in a dynamic, increasingly volatile market.

In short, the transition is no longer just a construction problem. It’s an operating system problem, and hiring is following that reality.

Watchlist for next month

- Finalisation of AEMO’s Integrated System Plan and implications for transmission priorities

- Further clarity on market design and pricing reforms affecting batteries and distributed energy

- Additional large-scale battery and hybrid project approvals as connection queues progress

Final word

The energy transition is no longer constrained by ambition, but by execution.

Prepared by Freshwater Group. Helping companies secure leadership and critical talent for the energy transition.

- Posted by Freshwater Group

- On May 1, 2026

- 0 Comment