Energy Transition Leadership Briefing | January 2026

Monthly Insights for Executives in Australia’s Clean Energy Sector

Opening Snapshot

January was a month of “the plan meets the invoice”. The energy transition narrative stayed broadly intact, but the practical constraints got louder: transmission cost escalation and sequencing risk; the growing weight of storage as the market’s shock absorber; and the still-underestimated complexity of coordinating REZ build-out, grid connection queues, and community/social licence.

Trendlines

System planning tightened around the Draft 2026 ISP and its implications for network build, firming and sequencing. (aemo.com.au)

Big transmission build milestones were celebrated, because transmission is now the transition’s pacing item. (energymagazine.com.au)

Utility-scale investment expectations for 2026 skewed heavily toward wind, underscoring the need to keep connection, approvals and supply chains moving. (pv-magazine-australia.com)

Large hybrid projects kept edging forward through approvals and grid approvals (solar + wind + BESS), showing where the market is heading: firmed renewables as the default shape. (pv-magazine-australia.com)

And RenewEconomy’s running commentary kept hammering the same point: politics and reliability narratives are being fought on the terrain of “spinning machines”, outages, and what “firming” really means in practice. (Renew Economy)

Highlights and lowlights

Highlights

- Draft 2026 ISP and regulatory scrutiny: AEMO’s 2026 ISP work program remains the central coordination instrument for NEM transition infrastructure, and the AER’s transparency review put formal pressure on assumptions, modelling and process quality. (aemo.com.au)

- EnergyConnect milestone: Transgrid’s EnergyConnect hit a major construction milestone, a tangible proof-point that big transmission can, occasionally, move from PowerPoint to steel. (energymagazine.com.au)

- Project pipeline continues to progress: Examples included Synergy’s major WA hybrid ambition clearing a key environmental hurdle, and additional solar+BESS projects achieving grid steps. (pv-magazine-australia.com)

Lowlights / friction points

- Cost, sequencing, and social licence risk (again): Planning certainty doesn’t automatically convert into build certainty, especially when transmission costs rise and delivery timelines collide with coal exit schedules. The ISP debate continues to orbit this tension. (Renew Economy)

- Reliability narrative pressure: Coverage continues to highlight the political and media potency of reliability events and coal outages, which shape stakeholder risk appetite and policy noise levels. (Renew Economy)

Policy and regulatory pulse

1) Draft 2026 ISP: the roadmap is still “Step Change”, but scrutiny is sharpening

AEMO’s 2026 ISP program is the primary “map” for least-cost transition pathways across generation, storage and transmission, and it remains the reference point for investors, networks and policymakers.

The AER’s January transparency review (and associated report materials) matters because it reinforces that the ISP is not just a planning artefact, it’s a regulated process subject to formal review expectations around transparency, evidence and modelling discipline. (Australian Energy Regulator (AER))

Implication: senior stakeholders should expect more contestability over transmission assumptions, option value, and the pace of coal retirements versus infrastructure readiness. That contestability is not a bug, it’s the system trying to price risk honestly.

2) Industry reaction: broad alignment on “renewables + storage + gas backup + networks”, but debate on costs and implementation

Industry commentary continues to frame the core transition recipe as settled, while the argument shifts to execution risk, cost allocation and consumer impacts. (energymagazine.com.au)

Implication: The policy fight is less “should we transition” and more “who pays, how fast, and what happens if the build slips”.

Grid and transmission

Transmission is the pacing item, and January’s coverage reflected it

EnergyConnect’s milestone (final towers, stringing completion) was positioned as a national-scale achievement because it directly addresses a core constraint: moving renewable energy across regions and improving interconnection resilience as coal exits. (energymagazine.com.au)

AEMO’s ISP work and ongoing discourse continues to revolve around the trade-off between:

- building major new high-voltage transmission, and

- getting more out of distribution-level hosting capacity and smarter network operations, and

- sequencing investment so the system does not overpay for stranded or delayed assets. (aemo.com.au)

Implication: expect more demand for senior “delivery integrators” who can bridge planning, approvals, construction and grid-connection realities.

Projects and capital signals

Hybridisation is the default: solar/wind with storage attached

Project updates reflected continued momentum toward large multi-asset developments:

- Synergy (WA) advanced a 2 GW solar, wind and battery ambition through a major regulatory hurdle. (pv-magazine-australia.com)

- Green Gold Energy (SA) reported grid connection approval progress for a 108 MW solar + 440 MWh BESS. (pv-magazine-australia.com)

These are meaningful because they show the market moving away from “energy-only renewables” toward “deliverable capacity-shaped renewables”.

Investment outlook: wind-heavy forecast for 2026 utility-scale spend

BNEF’s outlook (as reported) forecast $5.1B investment in Australian utility-scale wind and solar in 2026, with wind dominating the mix. (pv-magazine-australia.com)

- Late-2025 wind FIDs and turbine supply deals signal stronger construction starts in 2026. The investment drought for new wind projects in Australia is finally breaking.

Multiple wind projects reached financial close or locked in major turbine supply agreements in the last days of December, breaking a long drought of new FIDs and indicating a healthier pipeline moving into 2026, reinforcing OEM confidence and capacity commitment in the Australian wind sector ahead of construction starts.

Market structure and technology watch

Storage keeps moving from “adjunct” to “core market infrastructure”

Coverage across industry media continues to treat BESS as a central feature of system operation and investment strategy, rather than an experiment. (energymagazine.com.au)

At the same time, the ISP work and broader debate reinforces a basic reality: firming isn’t one technology, it’s a portfolio across batteries (various durations), hydro, demand response, network services, and sometimes gas.

Consumer energy resources still matter, but integration is the hard part

Even where uptake is strong, VPP participation, network integration and market design still determine whether “lots of batteries” becomes “a more stable and cheaper system”.

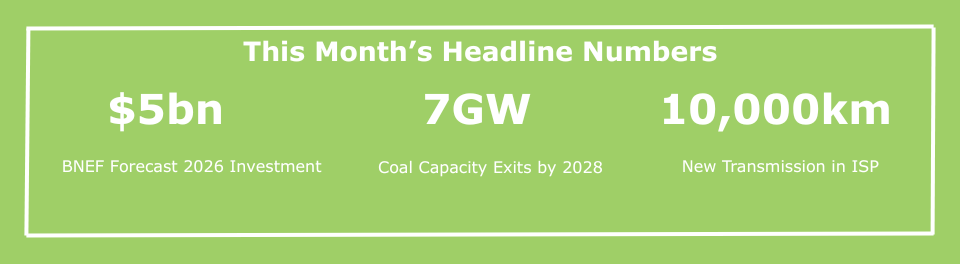

Data points

- $5.1bn

BloombergNEF forecasts $5.1 billion of Australian utility-scale wind and solar investment in 2026, with wind expected to dominate. This reinforces that transmission access and turbine supply, not capital availability, are now the primary gating factors for new build. - 7 GW of coal capacity exiting the NEM by 2028

Based on announced closures and ISP planning assumptions, around 6–7 GW of coal-fired generation is scheduled to exit the NEM by 2028, compressing timelines for replacement capacity and firming and increasing the delivery risk premium on projects that slip.

- More than 10,000 km of new transmission flagged in ISP pathways

AEMO’s Step Change–aligned planning continues to rely on over 10,000 km of new or upgraded transmission nationally over coming decades, underscoring why network delivery, approvals and social licence remain the critical path issues for the transition.

What this could mean for teams (hiring and org implications)

If January’s signal is “delivery friction is the story”, then hiring demand logically clusters around execution:

- Transmission & network delivery: program directors, construction managers, interface managers, land/approvals leads, and stakeholder/community engagement specialists (social licence is no longer a comms afterthought).

- Grid connection & power systems: grid studies, GPS compliance, commissioning, operational performance, congestion/curtailment strategy.

- Storage and hybrid operations: BESS engineering, trading/optimisation, asset management and performance analytics.

- Policy/regulatory and market design: roles that translate regulatory process into investment-grade decisions, especially as ISP contestability increases. (Australian Energy Regulator (AER))

Watchlist for February

- How debate around the Draft 2026 ISP translates into specific changes in assumptions and priority projects.

- Further evidence of transmission progress (or delays) across priority interconnectors and REZ-enabling works.

- Additional grid approvals and environmental milestones for large hybrid projects, especially those positioned to firm supply around coal retirement timelines.

Prepared by Freshwater Group. Helping companies secure leadership and critical talent for the energy transition.

- Posted by Freshwater Group

- On January 30, 2026

- 0 Comment